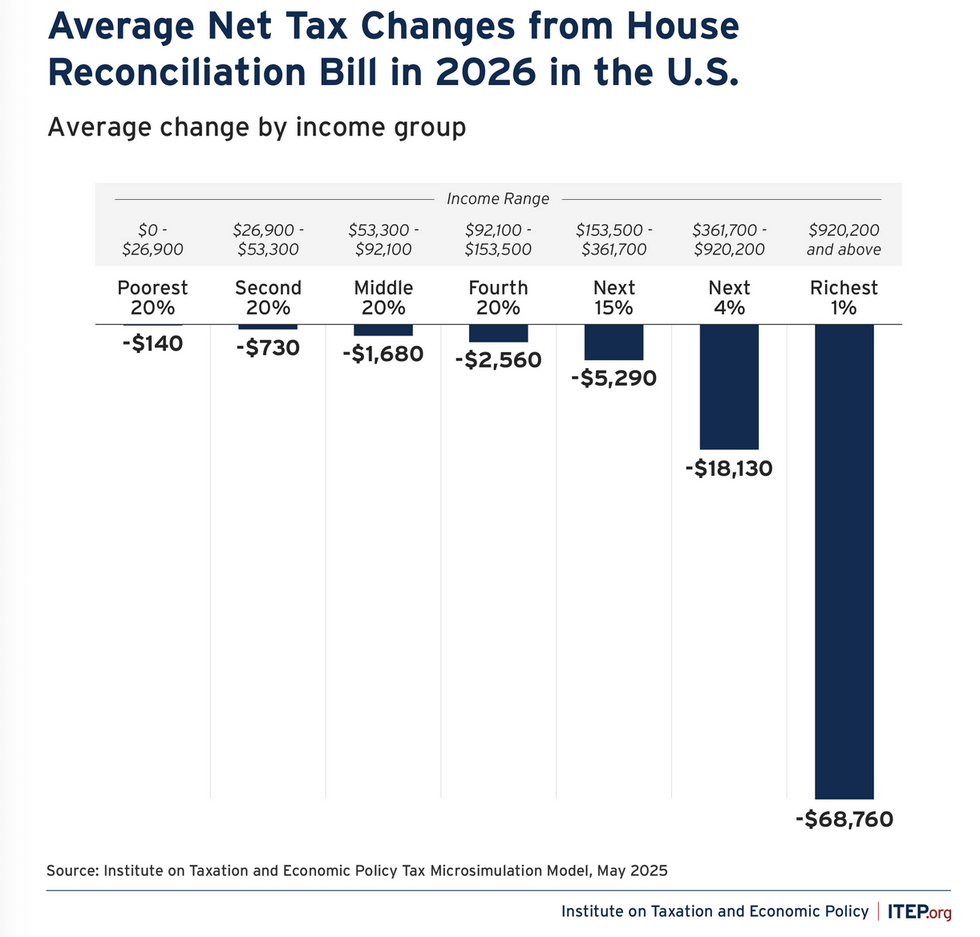

Contrary to proponents’ claims that the QBI deduction stimulates economic growth, economic research suggests a more nuanced and challenging reality. Recent analysis from our team at American University’s Institute for Macroeconomic and Policy Analysis (IMPA) reveals that extending or increasing the QBI is likely to exacerbate economic inequality, while delivering no economic benefits in the long run.

Extending the QBI deduction would systematically redistribute economic resources in ways that amplify existing inequalities.

Importantly, extending the QBI deduction would reduce government revenue significantly—by approximately 1.9% annually in the long run. Permanently increasing it would reduce revenue by 2.2% annually. These revenue losses represent a substantial fiscal challenge that cannot be overlooked.

Understanding Pass-Through Businesses

Traditional C corporations must pay the federal corporate income tax. Shareholders then pay individual income taxes on any profits distributed as dividends. In contrast, sole proprietorships, S corporations, and partnerships, as well as certain other types of businesses, are called “pass-throughs” because the businesses themselves do not pay taxes; instead, profits are passed through to individual owners, who then are taxed at their own individual tax rate. The QBI deduction reduces the amount of income from pass-throughs that is taxed.

According to Internal Revenue Service data, the number of nonfarm businesses organized as pass-throughs grew by 15% between 1980 and 2015, at which time more than 95% of all businesses were pass-throughs. But pass-through income is highly concentrated among top earners. Congressional Budget Office data show that, while income from pass-through businesses represents more than 20% of total household income for the top 1%, it accounts for merely 3% of income for the bottom 80% of households.

Think high-powered law firm partners or private equity fund executives. Without this tax break, they might owe the top marginal income tax rate of 37%. Under the current Republican proposal, they would owe just a 28.49% pass-through rate.

How Would Extending the QBI Deduction Affect the Economy?

Economic theory suggests that such tax deductions on business income have very little direct effects on real business activity if investment costs can be deducted from taxable income. And that is the case for pass-throughs. Because they can use accelerated depreciation provisions, taxes on their business income don’t change their investment decisions.

It’s not just theory: A recent study using tax record data finds no clear impact on investment, wages, or employment among pass-throughs that got an earlier tax break. A separate study found no impact on wages.

Even if tax breaks for businesses have no effect on individual business decisions, they can have negative effects on the economy as a whole. For example, such tax breaks reduce government revenue. If the revenue shortfall is financed by government borrowing, it can crowd out private investment. If the revenue shortfall is matched by reduced spending on public investment, such as scientific research, it is likely to reduce our standard of living in the long run. Such tax breaks also increase the after-tax required return to investors, which could cause businesses to distribute more profit, leaving less for investment.

We find that extending the QBI deduction would decrease government revenue by about 1.6% annually after 10 years and 1.9% in the long run.

Finally, such tax breaks increase after-tax profits and the market value of businesses, which raises the wealth of already-wealthy owners.

Our estimates using the IMPA macroeconomic policy model confirm that making the QBI deduction permanent would not boost economic activity, as is commonly claimed. Instead, we find that there would be a small decrease in GDP of 0.07% in the long run. Increasing the deduction to 23% would magnify the negative impact on economic activity.

Extending the QBI deduction would systematically redistribute economic resources in ways that amplify existing inequalities. Extending the QBI deduction would increase the share of the wealth owned by the top 1% by approximately 1.1%, while the bottom 50% would see their share fall by approximately 2.4%. Increasing the deduction, of course, redistributes even more wealth from the lower half of the distribution to the top.

Finally, we find that extending the QBI deduction would decrease government revenue by about 1.6% annually after 10 years and 1.9% in the long run. Increasing it permanently to 23% would reduce revenue 2.2% in the long run. How much is that? In the 2023 budget, 2% was enough to cover about three-quarters of the annual cost of the Supplemental Nutrition Assistance Program (SNAP). Or it would support 12 years of cancer research at 2023 levels.

To sum it up: QBI deduction costs taxpayers a lot, does not stimulate growth, and has regressive distributional consequences. There is no economic justification for its continuation.